What do Prince, Aretha Franklin and 60% of Americans have in common?

Recently, several celebrities have died intestate, meaning without wills – Prince, Aretha Franklin, Amy Winehouse, Jimi Hendrix, the list goes on… Similarly, several hadn’t updated their wills in several years, including Kurt Cobain and Heath Ledger. According to a survey from Caring.com, only 4 in 10 American adults have a will or living trust. This lack of planning can cause major turmoil with estates that are worth millions of dollars, but can likewise lead to conflict within families of smaller estates.

Failure of Prince and Franklin to leave a will caused tension within their families, particularly regarding rights to their music and songs. An added complication with celebrities’ estates is that they will oftentimes grow significantly after their death, which can make it difficult to determine how much their estate is worth. Additionally, the distribution process becomes very public.

Aretha Franklin died in August 2018 in Michigan and left four surviving sons. Since Franklin was not married at the time of her death, her estate will most likely be divided equally among her four living children, according to Michigan law. However, this process could take years and the amount of her estate will become public, according to law. It is unclear at this time the amount that Franklin’s estate is worth, but it is estimated at tens of millions of dollars. Creditors, to whom Franklin may owe debts, can also file claims against the estate to get their proper payments at this time. In addition, the IRS will have to be involved to ensure that Franklin paid all taxes that were owed. The IRS will then tax the remaining estate over $11.2 million at a 40% rate. This is known as the “death tax.” This process will be complicated and messy and may persist for years.

Another music legend, Prince, died in April 2016 in Minnesota without a will. After some initial disagreements about who his heirs would be, a Minnesota judge determined that Prince’s sister and five half-siblings are his heirs. This is because Prince was not married at the time of his death, did not have any living children at the time of death, and did not have living parents at the time of his death. Some suggest that Prince’s estate may be worth upwards of $300 million. There has been some reported disagreement between the siblings regarding what to do with Prince’s music, and in particular, the contents of the secret vault that was left at Prince’s mansion that is rumored to be full of unreleased music. Again, this has proved to be a complicated process, and still has not been finalized in the last two and a half years.

Although Franklin and Prince died in states other than Nebraska, both Michigan and Minnesota’s intestacy laws follow patterns similar to Nebraska. Even if you do not have a multi-million-dollar estate like Franklin or Prince, it is important to understand what may happen to your property if you die without a will and how this might affect your loved ones.

What happens if I die without a will in Nebraska?

When a person passes away, it is essential to look for their Last Will and Testament (will) to assist in the distribution of their estate and carry out their intentions. If the person dies without a will, the decedent is said to have died “intestate.” This means that the distribution of their estate will follow the Nebraska intestacy laws and will be distributed accordingly – which may or may not coincide with their wishes and protect their legacy.

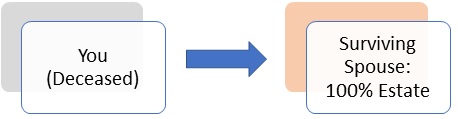

When there is not a will in place at death, the first step is to determine whether the decedent was survived by a spouse. The estate will first pass to the surviving spouse, if one exists. If there is a surviving spouse, and no lineal descendants of the decedent or parents of the decedent living, the entire estate will pass to the surviving spouse.

If there are surviving lineal descendants or children, who are all children of the surviving spouse as well, the surviving spouse will receive the first $100,000 plus one-half of the remaining balance of the estate and the lineal descendants will likewise receive one-half of the remaining balance of the estate.

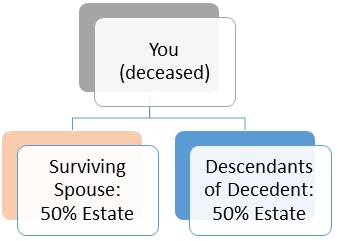

If there are lineal descendants, one or more of whom are not the lineal descendants of the surviving spouse, the surviving spouse and the lineal descendants (collectively) each receive one-half of the estate.

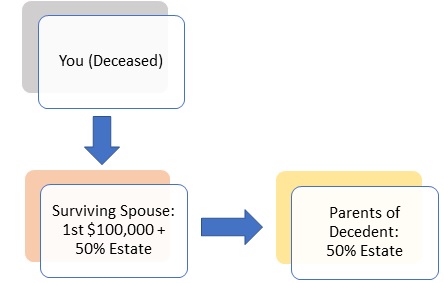

If there are no lineal descendants of the decedent, but the parents of the decedent are still living, the surviving spouse will receive the first $100,000 plus one-half of the remaining balance of the estate and the parents of the decedent will likewise receive one-half of the remaining balance of the estate.

If there is no surviving spouse, the lineal descendants will take. If there are no surviving lineal descendants, the parents of the decedent will take. If there are no surviving lineal descendants or surviving parents of the decedent, the siblings of the decedent and/or lineal descendants of the decedent’s parents (i.e., nieces, nephews, etc.) will take.

If there are no surviving spouse, lineal descendants, parents, or siblings of the decedent, one-half of the estate will pass to the paternal grandparent(s), if surviving, or to the lineal descendants of the paternal grandparents if both are deceased. The other half of the estate will go to the maternal grandparent(s), if surviving, or to the lineal descendants of the maternal grandparents if both are deceased. If none of the above are surviving at the time of decedent’s death, the entire estate will go to the next of kin in equal degrees. If there are no survivors of any degree listed above, the estate will pass to the state.

To summarize, the order of priority for intestate succession is as follows:

- Surviving spouse

- Children of the decedent or other lineal descendants

- Parent(s) of the decedent

- Lineal descendants of the parent(s) of the decedent (may include the decedent’s siblings, nieces, nephews, etc.)

- Grandparent(s) of the decedent

- Lineal descendants of the grandparent(s) (may include the decedent’s aunts, uncles, cousins, etc.)

- Next of kin in equal degree

After determining who will take from the estate, it must be determined what portion each person will take from the estate. Nebraska follows a distribution process called “modern per stirpes.” This means that the estate will be divided into as many shares as there are in the next generational level where there are still living descendants. For example, if the decedent has no surviving spouse and two surviving children, the estate will be divided equally, with one-half distributed to each child. Likewise, if the decedent has two children, four grandchildren, and both children have predeceased the decedent, the estate will be broken into as many shares as there are at the generational level where there are still living descendants. In this case, the estate would be divided into four equal shares for each living grandchild.

As a result of the “modern per stirpes” distribution process, grandchildren of the decedent may inherit unequal amounts if there are still living children of the decedent. In addition, certain grandchildren may not inherit anything if their parent is still alive. For example, if the decedent has two children, three grandchildren, one child is living and one child predeceased the decedent – one child will inherit 50% of the estate, two grandchildren will each inherit one-fourth of the estate, and one grandchild will inherit nothing. Below is a chart illustrating this example using the modern per stirpes system of distribution in accordance with Nebraska law.

In order to protect your legacy and carry out your intentions for distribution of your estate after your passing, it is critical that you create a will and execute any other necessary estate planning documents. For assistance with your estate planning or to learn more about Schmit Law Firm’s services, contact us at aschmit@schmitlawfirm.com or call (402) 979-6077.